RETIREMENT FOR ARTISTS

Rembrandt, Vermeer, and Van Gogh all died in poverty but with a little financial planning, you don’t have to.

Most of us don’t know anything about retirement. It’s rarely taught in school and when we do hear about retirement options, it always seems to target married couples with 9 to 5s and 401ks. If you are a self-employed artist, an employer provided 401k or 403b is probably not an option for you, but that doesn't mean you can’t still plan ahead for your retirement.

You can always keep money in a bank savings account, but your money likely will not keep up with inflation. Opening a retirement account is a great option for artists or any small business owners to plan ahead for their future.

Types of Retirement Accounts

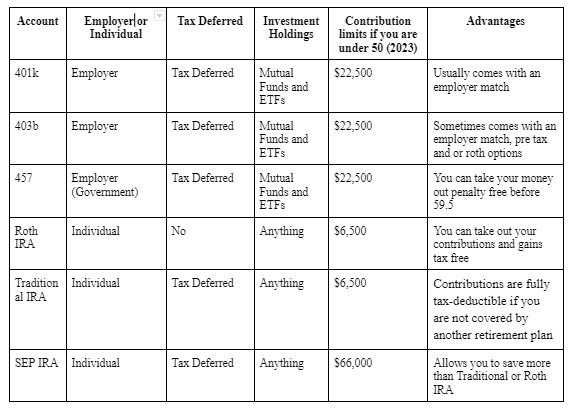

As an individually employed person without the benefit of an employer’s retirement plan, your options are a Roth IRA, a Traditional IRA, a SEP IRA, a Solo 401k, and a HSA. Some of these are additionally available to you even if you also have a 401k or 403B.

Let's look at what each one of these options are so you can choose what is best for you:

Roth IRA

An Individual Retirement Account is a personal account not tied to an employer. A Roth IRA isn’t itself an investment, but an account through which you can buy investments. Most Roth IRAs will give you access to a large investment selection, including individual stocks, bonds and mutual funds. The investments you select should be based on your risk tolerance and age.

A Roth IRA is good because you are paying taxes on what you put in. It grows but you don’t pay taxes on what you pull out. If you are in a low tax bracket now and think you will be making more money later in life, the Roth IRA is a great option because you pay low taxes on your contributions now, but won't have to pay taxes on your earnings when you take the money out years down the line.

Find what tax bracket rate you are in here:

A Roth IRA is the best deal for young investors and will have significant tax advantages over time. There are many places to open a Roth IRA such as Fidelity, Vanguard, or Betterment since they have a lot of high-quality low-cost investment options. It’s not necessary, but you might want to choose the same place you would also open a brokerage account for investing. Apps like Empower however, are great for managing your money even if you have accounts in many different places.

Another benefit of a Roth IRA is that you can pull out your contributions (the money you put in NOT your earnings) at any time, tax and penalty free. This will negatively affect your earnings in the long run, so it is not recommended, but good to know for emergencies! Once you reach age 59.5, you can withdraw the earnings tax and penalty free as well. The account must also be at least 5 years old by this time. As of 2023, Roth IRA max is $6,500 ($7,500 if you're age 50 or older), so this is what you should try to contribute every year.

Roth IRAs historically deliver between 7% and 10% in average annual returns. So, if you contribute $6000 a year starting at age 25, you will have around $1,146,940.00 by age 60, when the earnings can be collected tax and penalty free. That means retiring with approximately $38,231 a year if you live until 90 years old.

Calculate this for yourself here!

There are a few noteworthy exceptions that come with Roth IRAs that might be helpful to know. If you’re younger than 59½ and have owned a Roth IRA for less than five years, you can still withdraw some of your earnings for special circumstances. They are as follows:

Buying your first home.

Birth or adoption of a child.

Education expenses.

Unreimbursed medical expenses in excess of 7.5% of your adjusted gross income for the year.

Health insurance premiums while you’re unemployed.

The withdrawal is due to disability.

The withdrawal is made to a beneficiary or your estate after your death.

You decide to take substantially equal payments, which basically locks you into taking at least one distribution per year for at least five years or until you turn 59½, whichever comes last.

You made the withdrawal when you were a reservist, as defined by the IRS.

Generally you’ll owe income taxes and a 10% penalty if you withdraw earnings from your account, but if you withdraw because of one of the above exceptions, you can avoid the penalty, but not the income taxes.

If you’re younger than 59½ and you have owned a Roth IRA for 5 year or more, you can avoid taxes and penalties on earnings you withdraw from your account if you meet one of the following exceptions:

You’re withdrawing up to $10,000 to buy your first home.

The withdrawal is due to disability.

The withdrawal is made to a beneficiary or your estate after your death.

Traditional IRA

Traditional IRAs are taxed when the money is withdrawn, unlike Roth IRAs where the money is taxed going in. It is also good to know that contributions to a traditional IRA are tax-deductible if you are not covered by another retirement plan. A Traditional IRA might be a good choice if you believe you will be in a lower tax bracket (making less money) than you are now when it is time to retire. You can begin taking withdrawals from your Traditional IRA beginning at age 59 ½, with the distribution subject to ordinary income tax.

Whether you participate in a traditional IRA or a Roth IRA, you can contribute up to $6,500 per year, or $7,500 if you’re 50 or older to one or both combined - never exceeding the max per year. They are counted together so you cannot fill both with $6500 a year but you could put half in each if you wanted too.

Roth vs Traditional IRA

The biggest difference between a Roth IRA and a traditional IRA is how and when you get a tax break. Contributions to traditional IRAs are tax-deductible, but withdrawals in retirement are taxable. Contributions to Roth IRAs are not tax-deductible, but the withdrawals in retirement are tax-free. Do you think your tax rate will be higher or lower in the future? If you can answer that question, you can theoretically choose the type of IRA that will give you the biggest tax savings: If you expect to be in a higher tax bracket in retirement, choose a Roth IRA and its delayed tax benefit. If you expect lower rates in retirement, choose a traditional IRA and its upfront tax advantage.

If you think a Roth or Traditional IRA is right for you, consider putting investments into a target date retirement fund. These are offered just about anywhere you choose to open an account. The target date fund naturally adjusts your investment allocation between stocks and bonds as you get closer to retirement, so you don’t have to do much except keep putting money in! Another option is to invest your IRA in a mixture of low cost index funds which have lower fees over the long term, but a target date fund is a good place to start if you are new to investing or simply don’t want to think too hard about it.

SEP IRA

SEP-IRAs are primarily used by small-business owners who want to help their employees with retirement, but freelancers and the self-employed can also use this option. When you are a registered business owner and have more than the Traditional or Roth IRA limit to contribute, a Simplified Employee Pension IRA (SEP IRA) is a traditional IRA for self-employed people & small-business owners. It’s a retirement account that offers tax breaks for business owners and self-employed individuals who put money away for the future. If you have self-employment income, a SEP IRA will allow you to save more for retirement than either a Traditional IRA or a Roth. With a SEP IRA, you can contribute up to $66,000 in 2023, however the annual contribution limits cannot exceed the lesser of 25% of compensation. You can combine a SEP IRA with a Traditional or Roth IRA.

Generally, SEP IRAs are best for self-employed people or small-business owners with few or no employees because the IRS requires you to contribute an equal percentage of compensation to both your own retirement and that of your employees.

Contributions are tax-deductible, meaning they reduce your taxable income, and investments grow tax-deferred until retirement, when distributions are taxed as income.

Keep in mind, you must be a sole proprietor, business owner in a partnership, limited liability company, S corporation or C corporation, or earn self-employment income in order to qualify.

Solo 401k (or one-participant 401k)

A solo 401(k) is an individual 401(k) designed for a business owner with no employees. You can’t contribute to a solo 401(k) if you have full-time employees, though you can use the plan to cover both you and your spouse. There are no age or income restrictions and you can contribute up to $66,000 in 2023, with an additional $7,500 catch-up contribution if 50 or older.

In this type of retirement, you must think about yourself as both an employer and an employee. Within the overall contribution limit, your contributions are subject to additional limits in each role:

- As the employee, you can contribute up to $22,500 in 2023, or 100% of compensation, whichever is less. Those 50 or older can contribute an additional $7,500 here.

- As the employer, you can make an additional profit-sharing contribution of up to 25% of your compensation or net self-employment income, which is your net profit less half your self-employment tax and the plan contributions you made for yourself. The limit on compensation that can be used to factor your contribution is $330,000 in 2023.

Keep in mind that if you also have a 401(k) at another job, the limit applies to contributions across all plans, not each individual plan.

With a solo 401(k), you have the option to pick your tax advantage: You can opt for the traditional 401(k), under which contributions reduce your income in the year they are made. In that case, distributions in retirement will be taxed as ordinary income. The alternative is the Roth solo 401(k), which offers no initial tax break but allows you to take distributions in retirement tax-free.

Just like in choosing a Traditional vs a Roth IRA, a Roth is a better option if you expect your income to be higher in retirement. If you think your income will go down in retirement, opt for the tax break today with a traditional 401(k).

Sep IRA vs Solo 401k

SEP IRAs and solo 401(k)s both allow small business owners to establish retirement accounts for their employees, but SEP IRAs are funded by employer contributions alone. Solo 401(k)s allow both employer and employee contributions. As a qualified plan, 401(k)s come with rigorous reporting requirements while SEPs are relatively simple.

Solo 401(k) plans offer employee deferrals, catch up contributions for participants who are age 50 and above, and post-tax Roth contributions while SEP IRAs only allow traditional pretax contributions. Lastly, Solo 401(k) plans allow participants to take out a loan equal to the lesser of 50% of the plan balance or $50,000. Loans are not available with SEP plans.

HSA

HSAs are intended to pay for healthcare expenses, but they can be a valuable source of income once you retire. To qualify for an HSA, you need a health insurance plan with a high deductible.

HSA Contribution Limits for tax year 2021

- $3,850 for individuals

- $7,750 for family coverage

- $1,000 extra "catch-up" contribution if you're age 55 or older

In retirement, you can withdraw HSA money for things other than healthcare without incurring a tax penalty. Once you turn age 65, you can use HSA funds for any reason. You just pay ordinary income tax on the distributions.

A Very Brief Intro to Investing

Once you are all set up with the right retirement plan, and if you can to max out your contributions with some to spare, there is still more you can do to grow your money for the future. That of course is opening a taxable brokerage account. This can be done either through the same firm as your retirement plan, or you can go elsewhere. Betterment, Fidelity, and Vanguard are some options. I recommend also using an app like Empower, which will make tracking all your accounts (savings, retirement, brokerage) super easy. You’ll also see brokerage accounts referred to as taxable accounts, because investment income within a brokerage account is taxed as a capital gain.

Open a brokerage account and start investing. Everyone has different strategies and this will take a little of your own research but I personally like Index Funds and low cost ETFs (Exchange traded funds). Putting even just $100 a month in will see great rewards in the long run.

Remember that even a small difference in fees like .3%-1% can really make a massive difference in your investment returns over a long period and the time it will take you to hit your retirement goal. Any fee over 0.30% should be re-evaluated, since there are likely more affordable, but similar, investment options you could choose.

Conclusion

Planning for retirement as an artist or self-employed individual is not only possible but essential for securing your financial future. While historical examples like Rembrandt, Vermeer, and Van Gogh may remind us of the challenges artists have faced in their later years, today's options are far more diverse and accessible. From Roth IRAs and Traditional IRAs to SEP IRAs, Solo 401(k)s, and Health Savings Accounts (HSAs), there are various retirement account choices to suit your unique circumstances. Each of these options comes with its own advantages and tax implications, allowing you to tailor your retirement plan to your specific needs.

While it may seem daunting, remember that you can take it step by step. Assess your financial situation, explore your eligibility for different retirement accounts, and gradually build a retirement portfolio that aligns with your goals. By taking control of your financial future through planning and informed decisions, you can ensure that your retirement years are comfortable and fulfilling, even as an artist or self-employed individual. Don't let the misconception that retirement planning is only for 9-to-5 employees hold you back; your artistic journey can have a financially secure encore.

RESOURCES

Millennial Money

ChooseFI

Mr. Money Mustache

Free Tools tab at Dave Ramsey